Download the Policybazaar app

to manage all your insurance needs.

A guaranteed annuity is also called a fixed annuity, offering payments for a specified term or year. It continues paying a beneficiary or estate after the annuitant passes away. In some cases, the guaranteed annuity rate may fluctuate, but if your pension plan has a guaranteed annuity rate, your retirement income will generally be higher. Multiple factors affect this rate, including current market conditions, the surrender period, and the insurer’s policies. The key feature of guaranteed annuities is their reliance on present market values while promising predictable returns.

Get Guaranteed Lifelong Pension

For You And Your Spouse

Invested amount returned to your nominee

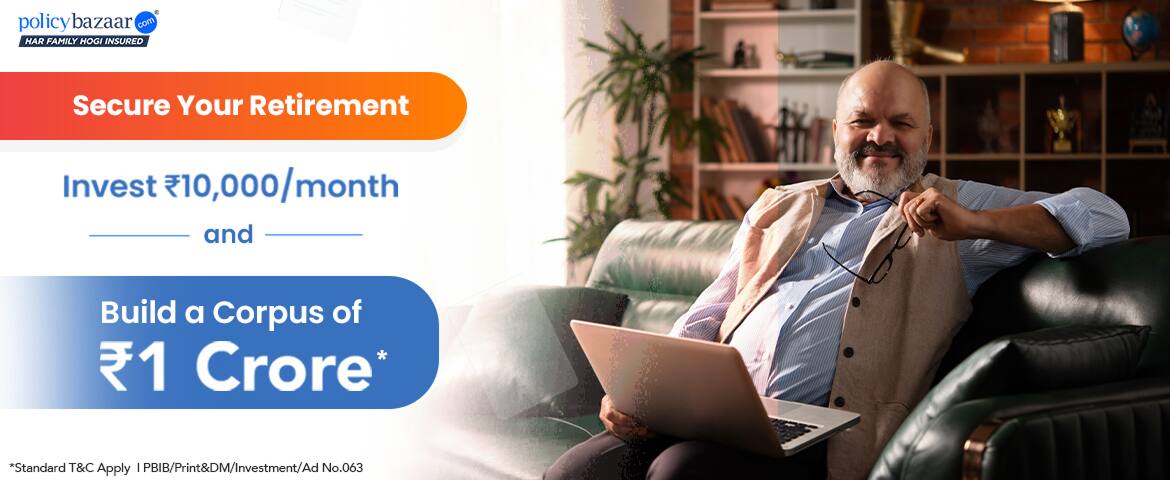

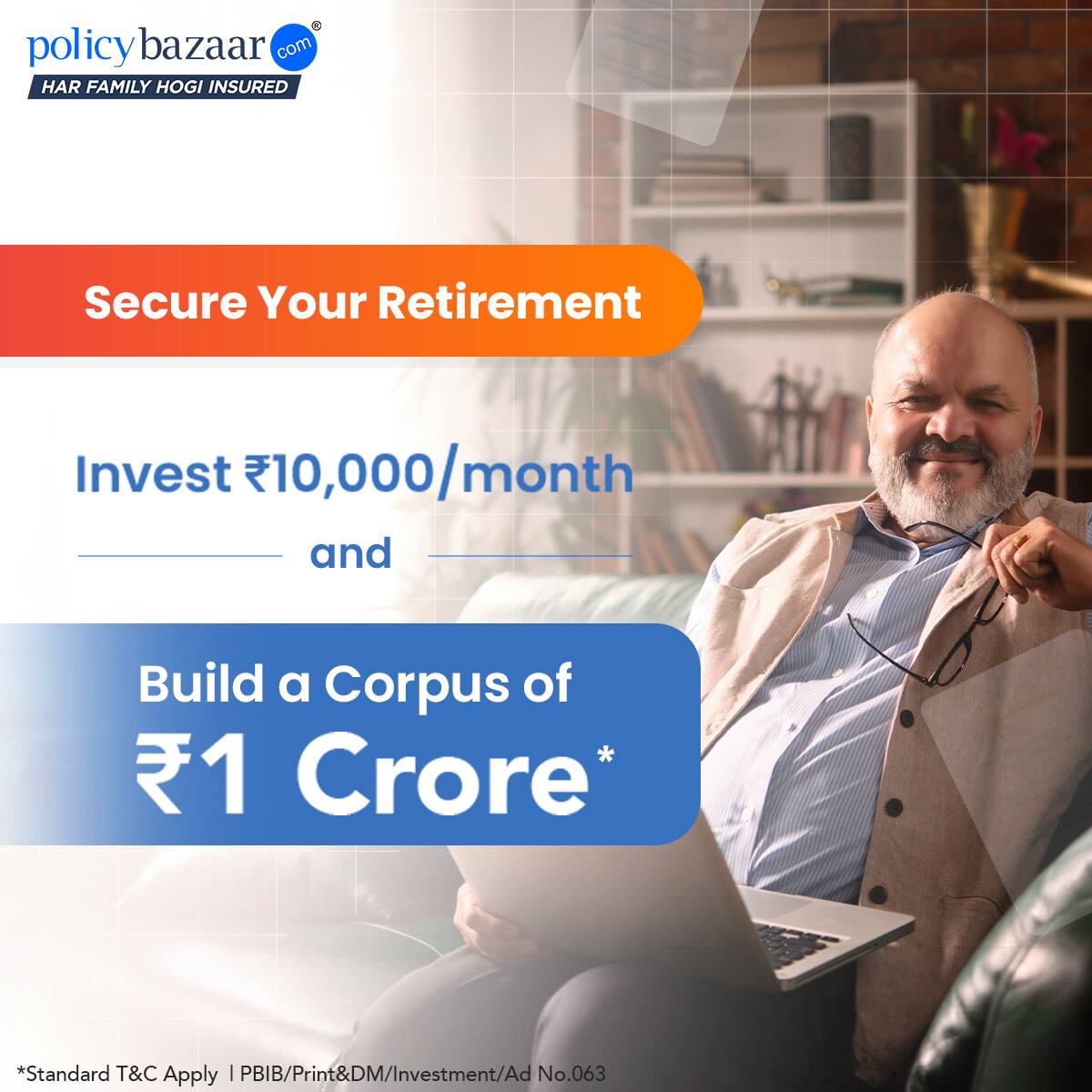

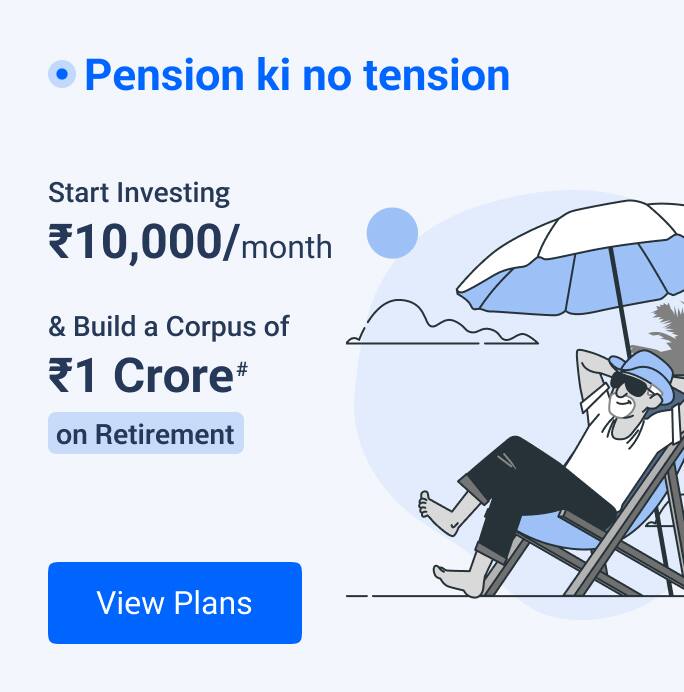

Invest ₹20k monthly & Get yearly pension of ₹4.2 Lacs for Life

Guaranteed Return For Life

Multiple Annuity Options

A guaranteed annuity rate ensures that you receive retirement income at a fixed percentage for a pre-defined period. It determines your return on annuity, irrespective of whether the annuitant survives the term.

These fixed annuity rates vary across insurers and often exceed the typical market rate available today.

For example, if the guaranteed annuity rate is 7%, an investment of INR 100 in a pension pool would yield INR 7 annually. It’s essential to review the terms and conditions of your guaranteed annuity carefully and ensure it aligns with your financial goals.

If you want to know whether your pension plan provides a guaranteed annuity rate, the process is straightforward.

If you have a guaranteed annuity rate, your pension provider must tell you of it. It happens between the times when you are near retirement and before you begin receiving pension payments. You can even request it to transfer elsewhere.

The insurer will generally give you a retirement income at different intervals after the age of 50. This should inform you whether you have access to any guaranteed annuity rates. You should carefully go through the plan conditions when you first join the pension plan.

Examine your document for terms like retirement annuity contract, Section 226 policy, with-profits, benefits, preferential, or guarantee. It is also a good idea to contact your pension provider directly.

Since return rates are not fixed, many consumers do not find their desired interest rate for these products.

In return for the insurance provider guaranteeing your principal plus a prefixed interest, you pay the insurance company a constant amount of money.

Your contract will specify terms such as how the money in your fixed annuity will increase. There are ways to achieve this, for example, interest rate or another contractual formula as per the contract.

A fixed annuity, often known as a life annuity, provides guaranteed lifelong payments. Based on the contract's terms outlining annuity payment options, you have to choose the number of years or the surrender period. Certain annuities or in other words, the term annuities, are those fixed annuity contracts that provide income benefits for a certain number of years.

If you are preparing for retirement, a guaranteed annuity may be an appealing option. Guaranteed annuities provide a steady source of revenue. You will know the interest rate and length of the interest on your money.

If you choose security and consistency above stock market gains, you can consider a guaranteed annuity. By covering future life expenditures, guaranteed annuities give financial security.

Guaranteed annuities are also good options for investors who want capital protection. In other words, those who want an investment return much greater than a savings account or certificate of deposit can invest in these annuities.

Annuities are only one of many retirement plans. You can be sure with a fixed annuity that they will give some security as they guarantee a rate of return.

Your payout is based on your age, account balance, and life expectancy. Though, you must pay taxes at standard income tax rates. Considering all these facts just mentioned you can pick the type of annuity that is best for you.

10 Nov 2025

The EDLI (Employees' Deposit Linked Insurance Scheme) is an

27 Oct 2025

The Atal Pension Yojana (APY) is a government-backed, voluntary*All savings are provided by the insurer as per the IRDAI approved insurance plan. Standard T&C Apply

++Source - Google Review Rating available on:- http://bit.ly/3J20bXZ

˜The insurers/plans mentioned are arranged in order of highest to lowest first year premium (sum of individual single premium and individual non-single premium) offered by Policybazaar’s insurer partners offering life insurance investment plans on our platform, as per ‘first year premium of life insurers as at 31.03.2025 report’ published by IRDAI. Policybazaar does not endorse, rate or recommend any particular insurer or insurance product offered by any insurer. For complete list of insurers in India refer to the IRDAI website www.irdai.gov.in

Insurance

Calculators

Payment Methods

Secured With

Follow us on